FNOL Automation in Insurance: How It Changes the Claims Journey from Day One?

The insurance claims journey often begins during one of the most stressful moments in a policyholder’s life. An accident, loss or unexpected event has already occurred and uncertainty is high. At this stage, how an insurer responds can significantly influence trust, satisfaction and long-term retention. This is why FNOL automation has become a central focus in modern insurance operations.

First Notice of Loss (FNOL) is no longer a simple administrative step. It is now a strategic entry point that affects the speed, accuracy and efficiency of the entire claims lifecycle. Insurers that modernize FNOL are not just improving how claims are reported; they are transforming how claims progress from first contact to final resolution. This guide explains FNOL automation in practical insurance terms and explores what truly changes once it is implemented.

What Is FNOL in Insurance and Why Is It So Important?

FNOL refers to the first instance when a policyholder informs their insurer about an incident that may result in a claim. This could involve an auto accident, property damage, theft or another covered loss. During FNOL, essential information such as incident details, policy references and initial loss descriptions are collected to create the claim record.

This stage matters because it sets the foundation for every step that follows. The quality of information captured at FNOL directly impacts claim routing, adjuster assignment, investigation timelines and settlement speed. Errors or omissions at intake often lead to rework, delays and increased operational costs.

For policyholders, FNOL is typically the first direct interaction with the insurer during a difficult situation. A clear, responsive experience builds confidence and reassurance. A slow or confusing one damages trust immediately. This is why FNOL is now viewed as a defining moment in the claims journey rather than a back-office formality.

What Is FNOL Automation in Simple Insurance Terms?

FNOL automation is the use of digital systems to capture, validate and route first loss notifications in a structured and consistent manner. Instead of relying on phone calls, emails or manual data entry, automated FNOL uses guided digital channels such as online forms, mobile interfaces and integrated systems.

The purpose of FNOL automation is not to eliminate human involvement. Rather, it reduces unnecessary manual effort at the intake stage while ensuring required information is collected accurately. Automation enforces structure, validates inputs in real time and prepares claims for faster downstream processing.

For insurers, this creates consistency and reliability at scale. For policyholders, it simplifies claim reporting and reduces uncertainty. FNOL automation supports human decision-making instead of replacing it, which is essential in insurance environments where judgment and empathy still matter.

How FNOL Automation Works in Practice?

FNOL automation typically follows a predictable and repeatable flow designed to minimize friction while improving data quality. Policyholders submit claim information through guided digital channels rather than unstructured communications. The system prompts for relevant details such as incident type, date, location and policy number.

As information is entered, automated validation checks ensure required fields are complete and formatted correctly. Once submitted, the claim is routed automatically to the appropriate team or adjuster based on predefined rules. Policyholders receive immediate confirmation that their claim has been recorded and is moving forward.

This structured intake process reduces delays, limits manual corrections and allows claims teams to begin evaluation with more confidence and clarity.

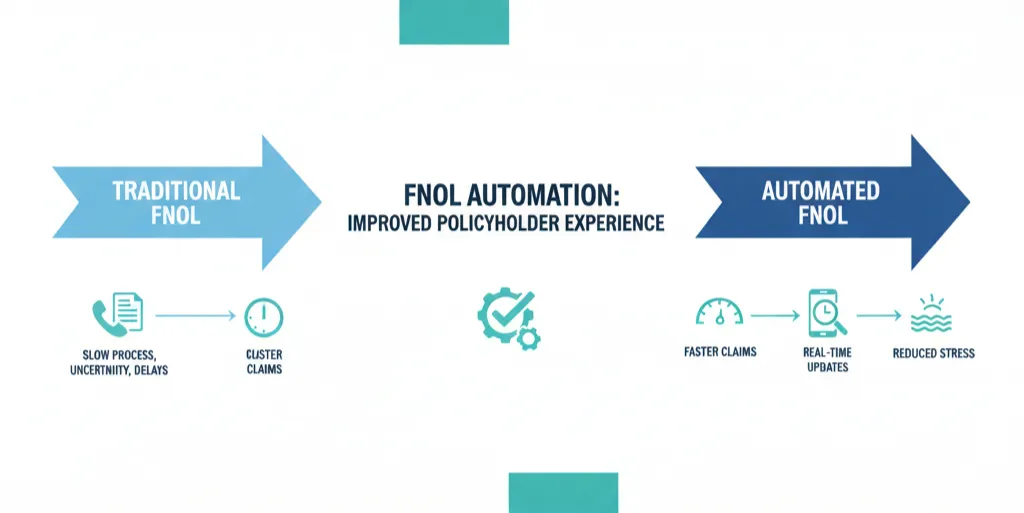

How the Claims Journey Looked Before FNOL Automation?

Before automation, FNOL relied heavily on manual processes. Claims were reported through call centers, emails or paper forms, often with inconsistent data capture. Information quality depended on individual handlers and follow-up calls were common to clarify missing details.

These manual workflows introduced delays at the very start of the claims lifecycle. Claims frequently sat in queues waiting for review. Adjusters spent time correcting intake errors instead of focusing on assessment and resolution. Visibility across teams was limited, especially during peak claim periods.

From the policyholder’s perspective, early communication was often slow and unclear. Even when claims were eventually resolved, the initial experience created frustration and negative perceptions that were difficult to reverse.

What Changes After FNOL Automation Is Introduced?

After FNOL automation, the claims journey becomes noticeably more structured and predictable. Intake happens faster because information is captured correctly the first time. Claims move into processing without waiting for manual sorting or clarification.

Claims teams experience fewer interruptions and receive more complete claim files. Managers gain earlier visibility into volumes, severity and processing status. For policyholders, acknowledgment is quicker and communication feels more transparent.

These improvements may seem incremental individually, but together they significantly reduce friction across the entire claims lifecycle and improve overall confidence in the insurer.

How FNOL Automation Improves Data Quality Across Insurance Operations?

Data quality is one of the most tangible benefits of FNOL automation. Manual intake often results in incomplete, inconsistent or unclear information. Automated FNOL addresses this by guiding how data is captured from the start.

Structured fields prevent critical details from being skipped. Validation rules catch errors immediately instead of days later. Conditional questions adjust based on claim type, ensuring relevance and clarity.

Higher-quality FNOL data reduces rework throughout the claims process. Investigations begin sooner, reporting becomes more reliable and compliance documentation is easier to maintain. In insurance, better data reduces operational risk and supports stronger decision-making at every stage.

How FNOL Automation Improves the Policyholder Experience?

FNOL automation changes how policyholders experience claim reporting. Instead of waiting on hold or repeating information multiple times, they can submit claims through guided digital channels at their convenience.

Immediate acknowledgment reassures customers that their claim has been received. Clear instructions reduce confusion and anxiety. Even when claims take time to resolve, a strong FNOL experience sets a positive tone that carries forward.

Over time, insurers that improve FNOL often see higher satisfaction scores because early communication builds trust during moments that matter most.

Common FNOL Automation Mistakes Insurers Make

Many FNOL automation initiatives underperform due to avoidable missteps. One frequent mistake is automating intake without redesigning workflows, simply digitizing old manual processes limits value. Another is forcing all policyholders into digital channels without offering assisted alternatives, which can reduce satisfaction.

Some insurers also underestimate change management. Claims teams may resist automation if it is positioned as oversight rather than support. Successful implementations involve adjusters early and frame automation as a tool that improves decision quality, not replaces expertise.

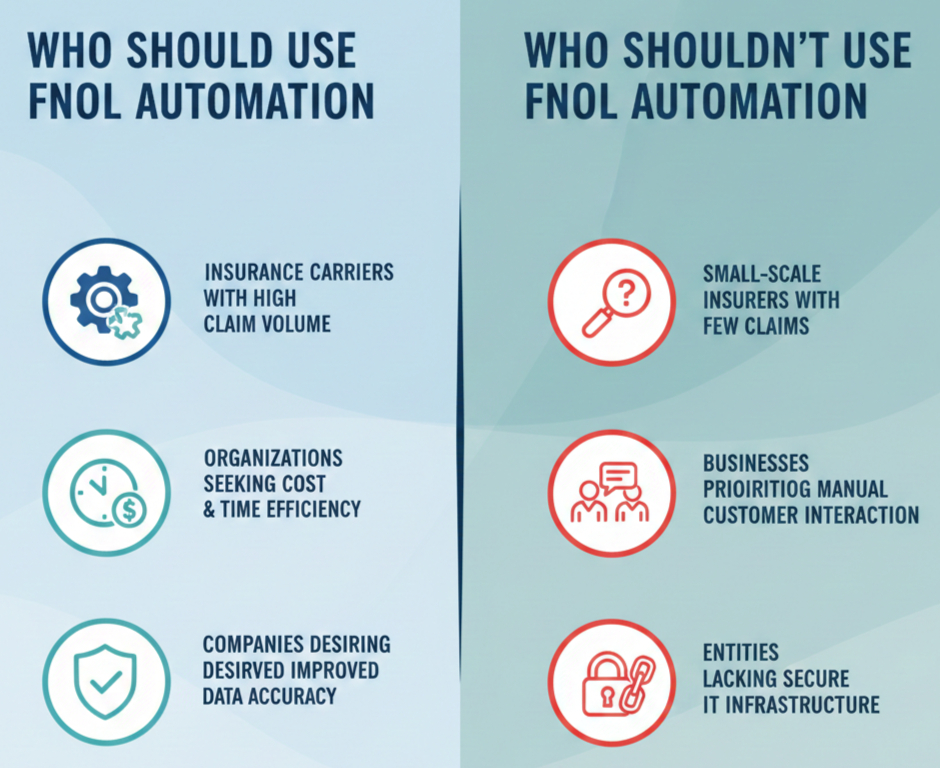

Who Should Consider FNOL Automation and Who Shouldn’t?

FNOL automation is not equally valuable for every insurer at the same stage of maturity. Understanding whether automation fits your operational reality is critical before adoption.

Insurers that handle moderate to high claim volumes, especially across auto, property or multi-line portfolios, benefit the most from FNOL automation. When intake volumes grow, manual processes introduce delays, inconsistency and avoidable rework. Automation creates structure and predictability that manual intake cannot sustain at scale.

However, FNOL automation may deliver limited value for insurers with very low claim frequency or highly bespoke underwriting models where every claim requires immediate human intervention. In these cases, selective automation rather than full FNOL digitization may be more appropriate.

This distinction is important because FNOL automation works best when it supports existing claims strategy rather than forcing operational change before the organization is ready.

When FNOL Automation Makes Sense in the Claims Lifecycle?

FNOL automation is most effective when introduced before downstream inefficiencies appear, not after claims teams are already overwhelmed.

Insurers typically reach this point when:

- Claim intake delays begin affecting customer satisfaction

- Adjusters spend excessive time correcting intake data

- Claims reporting lacks consistency across channels

- Compliance reviews surface documentation gaps

At this stage, automating FNOL delivers immediate operational relief because it improves data quality at the very start of the claims journey. Waiting too long often increases implementation complexity, as manual workarounds become embedded into workflows.

What FNOL Automation Does Not Fix?

One of the most common misconceptions is that FNOL automation alone solves all claims inefficiencies. It does not.

FNOL automation does not eliminate the need for skilled adjusters, improve poor policy wording or resolve settlement disputes. It also does not automatically detect fraud or guarantee faster settlements in complex claims.

What FNOL automation does provide is a cleaner, more reliable starting point. It ensures claims begin with accurate, structured information, allowing downstream processes to perform better. Insurers that treat FNOL automation as a cure-all often become disappointed. Those that treat it as a foundation see long-term value.

Early Risk and Compliance Advantages of FNOL Automation

Structured FNOL data allows insurers to identify risk and compliance issues earlier in the claims lifecycle. Claims with unusual patterns or missing details are flagged sooner, enabling faster review. High-severity cases are prioritized more accurately and documentation is captured consistently for audit purposes.

Compliance teams gain clearer visibility into intake practices, reducing the likelihood of regulatory surprises later. Early identification allows insurers to manage risk proactively rather than reacting after issues escalate.

What Insurers Typically See in the First 60 Days?

Within the first 60 days of implementing FNOL automation, many insurers observe measurable improvements. Intake times shorten, data errors decline and claims are routed more efficiently. Adjusters report fewer clarification requests and customer inquiries decrease because acknowledgment happens faster.

Managers benefit from clearer performance tracking and earlier insights into claim trends. These early gains explain why FNOL is often the first process insurers choose to automate.

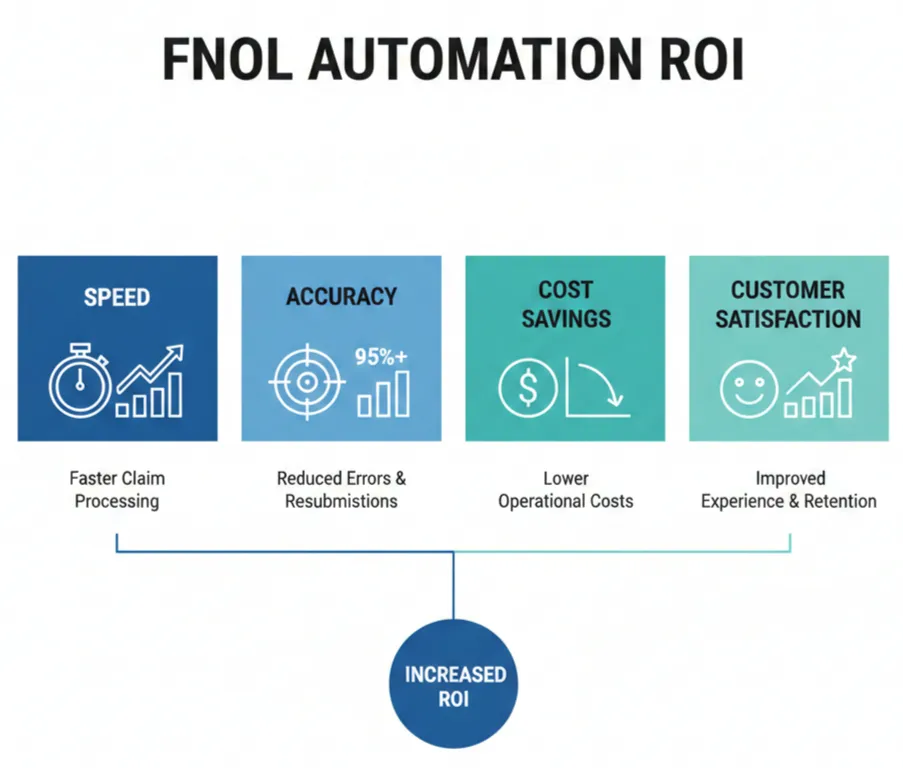

How Insurers Measure ROI from FNOL Automation?

Return on investment from FNOL automation is typically evaluated using both operational and experience-based metrics. Insurers track FNOL-to-acknowledgment time, data correction rates, customer satisfaction scores, cost per claim and compliance incident frequency.

Comparing these metrics before and after automation helps insurers understand value beyond technology adoption. Improvements in speed, accuracy and trust all contribute to long-term operational efficiency.

Common Challenges When Implementing FNOL Automation

FNOL automation is not without challenges. Some policyholders still prefer traditional reporting channels. Internal teams may initially resist new workflows. In some cases, automation tools are deployed without proper alignment to existing processes.

Successful insurers address these challenges gradually. They support multiple intake channels during transitions, train teams using real claim scenarios and refine workflows continuously. FNOL automation works best when treated as an evolving capability rather than a one-time implementation.

Frequently Asked Questions About FNOL Automation

Is FNOL Automation Worth It for Small and Mid-Sized Insurers?

Yes, FNOL automation can be valuable for smaller insurers when implemented at the right scale. Modular or phased automation allows insurers to improve intake accuracy without large system overhauls. Even limited automation reduces rework, improves compliance and creates a more professional claims experience.

Does FNOL Automation Increase Claim Processing Speed?

FNOL automation improves processing speed indirectly by eliminating intake delays and data errors. While it does not settle claims automatically, it allows adjusters to begin evaluation sooner with better information, which shortens overall cycle time.

How Long Does It Take to See Results from FNOL Automation?

Most insurers see measurable improvements within the first 30 to 60 days, particularly in acknowledgment time, intake accuracy and reduction in follow-up requests. Early gains occur because FNOL impacts every claim, regardless of complexity.

Is FNOL Automation Secure and Compliant?

When designed properly, FNOL automation strengthens compliance. Structured data capture ensures consistent documentation, supports audit readiness and reduces reliance on untracked communications such as emails or handwritten notes. Security depends on system governance rather than automation itself.

Does FNOL Automation Replace Human Decision-Making?

No. FNOL automation supports human decision-making by removing manual intake burdens. Adjusters remain responsible for evaluation, negotiation and settlement decisions. Automation enhances judgment by improving information quality.

Conclusion: Why FNOL Automation Matters in Modern Insurance?

FNOL automation changes more than how claims begin. It improves how claims move, how teams collaborate and how policyholders feel during difficult moments. By structuring intake, insurers gain speed, clarity and confidence across the entire claims journey.

If your organization is evaluating FNOL automation or looking to strengthen early-stage claims performance, understanding how to apply it thoughtfully is essential. To explore how smarter FNOL strategies can support your insurance operations, visit amityfin.com or speak directly with our team at +1 (888) 914-8699.

Recent posts

-

Digital Transformation in Insurance: How Technology is Reshaping the Future of the Industry

05 Feb, 2026 -

AI Auto Insurance: How Artificial Intelligence is Revolutionizing Car Insurance in the USA

05 Feb, 2026 -

Insurance Automation System: How Automation Is Transforming the Insurance Industry?

22 Jan, 2026